New research from Omdia says Southeast Asia’s smartphone market fell 9% year-on-year in the first quarter of 2026, with shipments totaling 21.6 million units, while average selling prices rose to a record $349—up 19%—as vendors sought to protect margins amid higher memory costs.

Omdia said the combination of lower volumes and higher prices indicates a “structural repricing” across the region, driven by DRAM and NAND cost inflation. The firm warned that affordability pressures are rising in a price-sensitive market where more than 60% of smartphones are priced below $200.

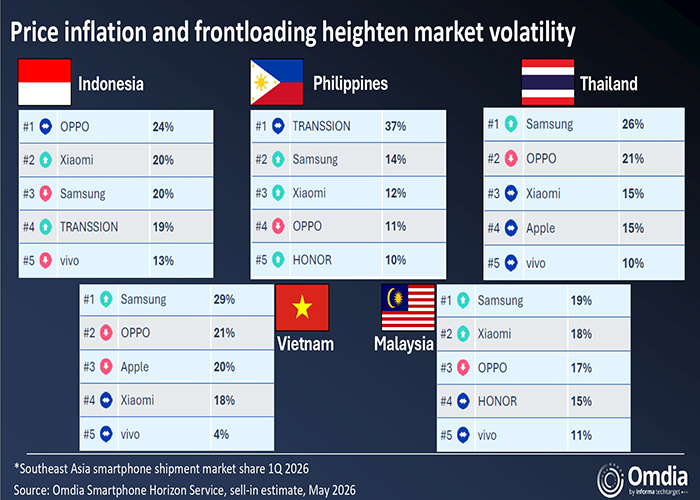

On vendor rankings, Omdia said Samsung led Southeast Asia in 1Q26 with 4.6 million units and a 21% share, up 4% year-on-year, which it attributed to the S26 launch and A-series volumes. OPPO was second with 4.2 million units, down 17%, which Omdia linked to operational adjustments following its combination with realme. Xiaomi placed third with 3.7 million units, down 12%, which Omdia said reflected portfolio-wide price increases that reduced channel demand. Transsion ranked fourth with 3.4 million units, down 10%, supported by Infinix and Tecno models in Indonesia and the Philippines. Vivo completed the top five with 2.1 million units, down 27%, as it shifted away from the entry-level segment to focus on profitability. Apple ranked sixth at 1.8 million units, broadly flat year-on-year, while HONOR grew 28% to 1.2 million units, which Omdia said was the strongest performance among tracked vendors.

“The defining story of 1Q26 is ASPs reached an all-time high while volumes declined — and the two trends are closely linked. Memory cost inflation has raised device bill of materials (BoM) across the board, particularly in the entry and mid tiers where DRAM and NAND account for a larger share of total component cost. In response, vendors have raised prices and, importantly, managed supply more tightly to prevent channels from reverting to legacy discount levels.

For a region where the sub-$200 segment still account for the majority of volume, this creates a difficult balancing act: vendors must either pass through costs on to consumers, absorb margin compression, or reduce specifications and risk volume erosion. Each option carry trade-offs,” said Omdia Research Manager, Le Xuan Chiew.

Omdia said the region’s overall market value grew 8% despite the 9% shipment decline, suggesting growth was driven by repricing rather than an expansion in demand. It added that vivo and OPPO recorded the strongest average selling price growth among major vendors at 28% and 26% respectively, reflecting a shift away from low-margin entry-level shipments. In contrast, Omdia said HONOR and Samsung pursued market share gains through brand and channel investment.

The research pointed to product strategy changes in Malaysia as an example of how vendors are adapting to component inflation. Omdia said Xiaomi increased the price of the Redmi Note 15 4G to RM799 from RM699 for the Redmi Note 14 4G, while the 5G model maintained its RM899 price point but shipped with lower RAM and storage. It added that the Redmi Note 15 Pro+ launched with a higher memory configuration, with a 12GB/512GB variant priced at RM1,899 compared with RM1,599 previously.

In Singapore, Omdia said HONOR rose to third place for the first time, supported by retail execution and mid-range momentum, particularly for the X9d. It said the second half of 2026 will test whether volume-led strategies remain viable if bill-of-materials costs continue to rise.

At the country level, Omdia said Indonesia—the region’s largest market at 7.2 million units—recorded a 17% year-on-year decline as channel inventory normalized from 4Q25 and consumers remained cautious amid higher prices. It added that demand was also affected by a weaker-than-expected Ramadan season and recent retail price increases. Thailand posted 2% growth, which Omdia attributed to Samsung’s positioning in premium and upper mid-range devices. Vietnam and Malaysia declined 12% and 19% respectively, which Omdia said was driven by a shipment contraction of more than 30% in the sub-$200 segment.

“The country-level picture was more mixed than the regional headline suggests. Indonesia, the region’s largest market at 7.2 million units, recorded the steepest absolute decline, falling 17% year-on-year as elevated channel inventory from 4Q25 continued to normalize and consumers remained cautious amid persistent price pressure. The weakness was further exacerbated by a softer-than-expected Ramadan season and recent retail price increases, both of which weighed on replacement demand. Given Indonesia’s strategic importance to most Android vendors, the market slowdown had an outsized impact on their overall regional performance.

Thailand remained relatively resilient, posting 2% growth, supported by Samsung’s stronger positioning in the premium and upper mid-range segments, which helped offset continued softness in entry-level demand. Meanwhile, Vietnam and Malaysia declined 12% and 19% respectively, driven by a severe shipment contraction of more than 30% in the sub-$200 price segment,” said Omdia Senior Analyst, Sheng Win Chow.

Looking ahead, Omdia said pricing and supply volatility is likely to persist as vendors balance supply shortages against the demand impact of further increases, noting that channels in several key price segments have moved from overstocked to understocked, giving vendors greater ability to enforce pricing discipline.